Economists and their forecasts are notorious for not forecasting important turning points in the economy and financial markets. These forecasts are constantly updated, and the updates are probably more important as I can track the trend in the changes, are they improving, deteriorating, or staying the same. This is why I also do a monthly market forecast. The outlook can help us be more aggressive, or more cautious.

The forecasts, estimates below are a consolidation from 2017 outlooks from Barron’s, WSJ, Fortune, BusinessWeek, CNBC, Wells Fargo, Charles Schwab, Merrill Lynch and our analysis of economic, business, and investment trends.

Summary

- Investors, traders and some analysts are bullish on the incoming administration’s pro-growth, pro-business approach for the country.

- Even though investors are enthusiastic, most analysts have barely increased their 2017 estimates for GDP and earnings.

- The U.S. economy is basically in good shape and does have tailwinds: low inflation, job growth, high consumer and business confidence, and anticipated increased capital spending. The U.S. economy is expected to continue to grow in 2017.

- If 2017 turns out to grow and the bull market continues, this would be one of the longest economic expansions and bull markets on record.

- Most economists, and analysts have low expectations for the global economy and markets.

- Earnings are expected to increase in 2017. I will write more about this in my 2017 market outlook that should be out in about a week.

- There are risks to our economy and markets, and most of these risks are external. One of the main risks is a slow global growth economy, especially China, Japan and Europe, a stronger dollar, and potential conflicts with our trading partners.

- It seems as though many investors and analysts are not concerned about the incoming President’s personality, many outside of Wall Street are concerned.

As an investor, I’m concerned about the expensive valuations of the markets, stocks. I’m being very selective, but also being patient and disciplined.

I will have my 2017 market outlook soon.

GDP

The U.S. economy has averaged about 2% growth for this economic cycle that started in 2009.

The charts below includes an average 2017 GDP forecast from aproximately 60 economists:

These forecasts are constantly updated. The red lines are the estimates. The gray columns are the actual growth rates. Again, it’s important to track the change in forecasts.

The consensus GDP forecast for 2017 is about 2.4% growth.

Most economic cycles last about 5 years. If this cycle ends in 2017, this economic cycle would be an unusual 8 years. An economy that has grown 8 years without a recession is a very good thing.

During the Presidential Campaign, President-Elect Donald Trump said his goal was to ramp up GDP growth to 5% to 6%. Economists are forecasting much lower. They are waiting to see what will be passed by lawmakers and when. Also, once passed, the effects won’t be felt until later in 2017, and 2018. The forecast for 2018 is also 2.4%.

I believe it will be difficult to have a sustained growth rate above 3%. I wrote a research report about this slower growth, The New Normal Update. Click here to read the article. The article explains why the U.S. has and will probably continue to have a slow growth economy. The article is partly based on the book When Markets Collide by Mohamed El-Erian.

There are concerns for 2017:

- Inflation is expected to increase

- Interest rates are rising

- Oil prices are higher

- The dollar has risen sharply

- A global economy that has slow growth

- Geopolitical hotspots and threats

- Overvalued stocks and markets

Most of the headwinds the economy faces are external, and that I will review in the Global Concerns section below.

Most economists don’t expect a recession for 2018:

As I mentioned above, economists and analysts don’t have a good track record of calling important turning points in the economy and markets. In January 2008, the forecast for a recession was only 30%; one year later the forecasts jumped to 100%, when we were in a recession. Admittedly, forecasting the future is extremely difficult.

Recession probabilities did move up last year and have fallen a bit the last few months.

Here is the consensus forecasts’ for unemployment:

The unemployment rate fell about 50% since the start of the Great Recession. Full employment is considered about 5%, so we’re at full employment.

Unfortunately some in the labor force have part-time and many would like to work full time. Also, many new jobs are in low paying service jobs in the lodging and restaurant industries.

Economists expect the unemployment rate to stay at these lower levels for the next few years.

Consumer

The consumer is about 70% of the economy, and the consumer is in good shape.

There have been several decades of wage stagnation, as the chart below shows:

As the chart below shows, we are finally starting to see wage increases:

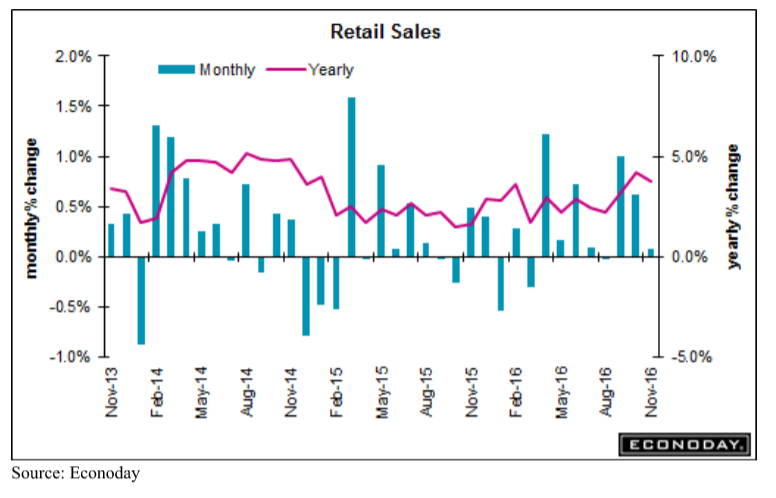

Consumer confidence, wages, employment trends are all improving, so retail sales, real estate and autos all had a good 2016.

Retail sales are essentially fine, but because of higher interest rates and stretched consumers, some economists are concerned about housing and autos – two important industries in our economy.

Oil

The Saudis and OPEC finally cried uncle and have decided to cut oil production. Russia also agreed to production cuts, even though they are not part of OPEC. Lower supplies leads to higher prices.

Oil prices fell below $30 in early 2016. If you’ve studied oil, you knew prices would not stay this low for long because there would be no incentive to look for oil. Once you’ve used a barrel of oil, it needs to be replaced, and as time goes on, exploring and developing oil becomes more difficult and expensive. If prices would not have increased we probably would have had shortages, especially if there were supply disruptions from terrorist attacks, wars, hurricanes, oil spills, labor strikes, maintenance issues….

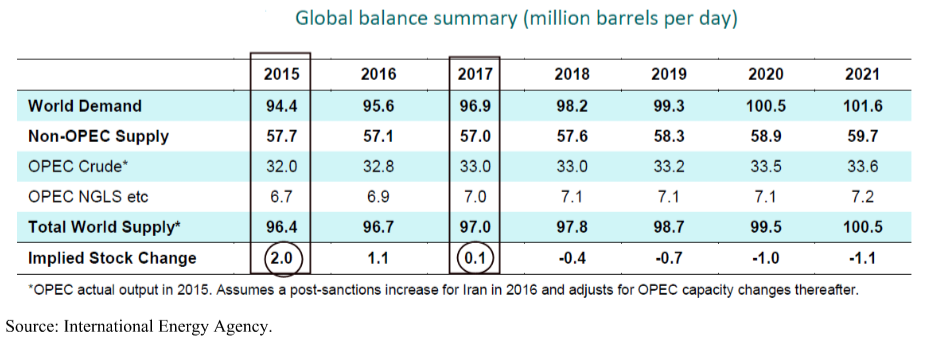

Below is a global oil supply, demand table:

In 2015, global oil demand was 94.40 million barrels a day, and supply was 96.4, a 2 million barrel a day surplus.

Forecasters see oil demand increasing to 96.9 million barrels a day in 2017, leaving a small surplus of only .1 million barrels a day.

The forecasts do see shortages in 2018 and beyond. In 2020, demand is expected to be over 100 million barrels per day.

Below is the consensus oil price forecast for 2017:

The current consensus forecast for oil is about $56 for 2017. Relatively low compared to most of this decade.

Inflation

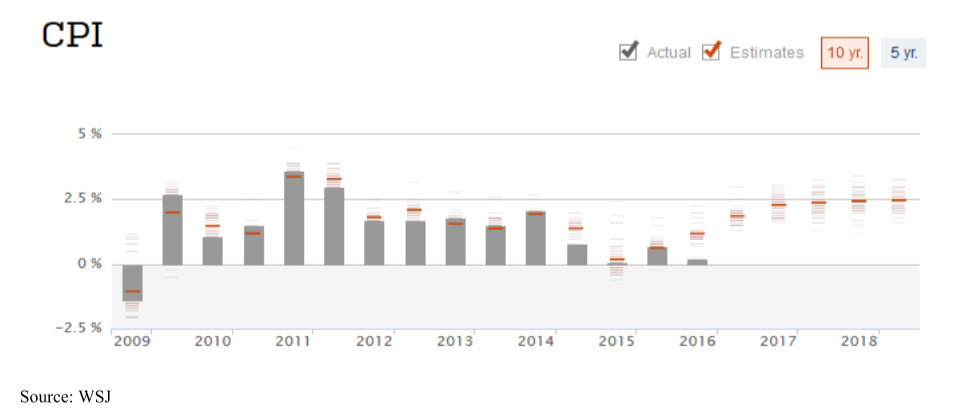

Below is a chart that shows the trend and 2017 forecast for inflation:

Inflation has been about 2% for much of this cycle, and has been below that the last few years.

Economists see inflation rising due to rising oil prices, wage increases, and a shift from monetary policy (money supply and interest rate focus) to fiscal policy (government spending, taxes).

Interest Rates

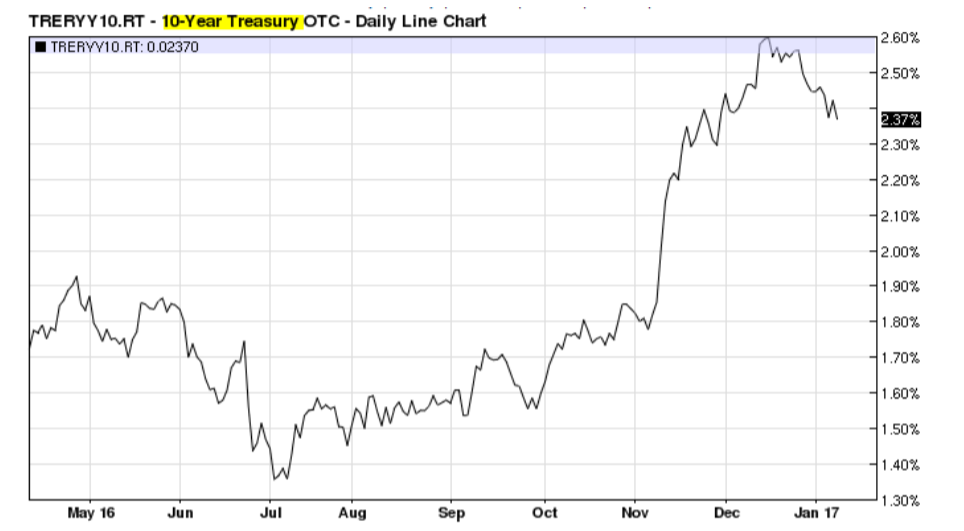

Because inflation is expected to increase, interest rates are increasing. Below is a chart for the 10-Year Treasury:

We can see that rates spiked after the election. The 10-Year Treasury fell below 1.4% last summer, and the yield almost doubled to 2.6% recently. As mentioned above, rising rates could lower activity in housing, autos and other big ticket purchases that need borrowing for consumers and businesses.

The Federal Reserve is expected to raise rates about two to three times in 2017. Below is the consensus Wall Street forecast for the federal funds rate:

For most of this economic, interest rate cycle, the federal funds rate had been .25%. This forecasts sees the federal funds rate at about 2% next year.

Below is the forecast for the 10-Year Treasury:

Economists see the 10-Year at 3.23% by the end of next year. The increase in rates could be disruptive to the markets and economy, even though historically 3.23% is relatively low.

Global Concerns

I’ve been watching global oil markets for several decades, and when I read domestic oil reports or listen to cable financial news, the perspective and analysis is U.S. centric - this is a mistake. We still import much of our oil needs, so analysis needs to include the global outlook.

Last year many analysts felt that oil prices would remain depressed because they focused on U.S. demand and supply where the energy outlook is healthier. But as the global oil supply, demand table above shows the outlook is much different. Because I look at global supply, demand data, I was not surprised to see oil prices move higher. I also understood that OPEC, especially Saudi Arabia could cut oil production at any time causing oil prices to move higher. They were increasing production the last two years to keep oil prices low, and now they will be cutting production.

Investors make the same mistake by being too U.S. centric, and do not pay attention to the many risks that the global economy faces. Yes, the U.S. outlook looks good, but outside our border there are many risks.

China

China faces too much debt, bad capital allocation, a slowing economy, a weak currency, and capital is leaving the country. Also, the President-Elect may challenge China regarding many of its policies, especially regarding trade.

Below is a chart that shows the alarming rise in their debt and money supply:

The increased debt has not helped China’s growth and is an indication of bad capital allocation as the chart below shows:

Even though China has increased lending, it has not helped economic growth

Below is a chart that shows where much of the money has gone:

The most dramatic increases in spending are in SOEs (state-owned enterprises) and government spending.

One of the other major problems facing China is a weakening currency and capital flight:

China’s foreign exchange reserves peaked in 2013 and has been falling since. Their currency has been falling, and now they have a problem with capital leaving the country. They’ve been spending some of their reserves to keep their currency from going lower.

I’ve written about the China economic and commodity boom reversal. Click here to read my November Economic Outlook for 2013. The China and commodity reversal continues to play itself out.

One of the biggest concerns among investors and economists is a potential trade war with China. A trade war with China could lead to a global recession. Wilbur Ross, the pick for Commerce Secretary stated on a financial news channel that trade tariffs would be a last resort and that he would be a buffer between the President elect and China and our other trade partners.

Wilbur Ross is a billionaire business man who is known as a turnaround expert for struggling and bankrupt businesses.

European Union

Since the global financial crisis of 2008, Europe has had crisis after crisis:

- Grexit

- Brexit

- An influx of millions of refugees from the Middle East and Africa

- Terrorist attacks

- Slow growth

- The European Union has been struggling to financially and politically integrate its 28 sovereign countries.

- A banking system that has questionable reserves and financial soundness.

- Many important countries in the world are embracing nationalism including Britain, and the U.S. Italy voted against reforms to be more globally competitive late last year. Germany, France, Netherlands, Norway, and Czech Republic will be having general elections. Some of these countries may also vote to become more nationalistic.

The rejection of globalism by more countries could hurt the global economy.

Below are a few charts that partly explain slow global growth:

As countries become more nationalistic, global trade could suffer more.

Low productivity can effect standard of livings, and inflation.

Slowing global capital spending sometimes mean businesses don’t feel confident with current and future business conditions.

Middle East and North Africa

The Middle East and its plentiful and low cost oil reserves are important to the global economy, but it has also been a source of instability, wars and global terrorism.

Syria, Iraq, Iran, Libya, and Afghanistan remain dangerous, and their instability, terrorist attacks and wars could lead to oil supply disruptions, or worse more wars.

My question: can the U.S. remain an island of prosperity, with a slow global economy and high geopolitical risks.

Black, Grey Swan Events

There are always the “black swan” events that are improbable, and unknown but could have a big impact.

These could include Venezuela’s economy collapses. We get about 9% of our oil imports from Venezuela.

Also, Mother Nature and weather have been responsible for crises around the world.

The President Elect has some personality quirks that could get the U.S. in trouble militarily and financially.

New President and Administration

Investors are very enthusiastic regarding the new administration led by many successful business and Wall Street leaders. It is very rare that the government is run by business leaders. Below is a table that shows which administrations had the most business experience, and GDP growth associated with those administrations:

As the image above shows, President Trump will have more business experienced people versus government/military experience in his administration. There does not seem to be a correlation between GDP growth and a pro-business administration. Both Bushes had administrations that had a lot of business experience, but GDP growth was anemic. To be fair, both Bushes had wars in the Middle East that partly caused recessions in both Bush terms.

One of my concerns that I have that is rarely mentioned in the financial media is President-Elect Trump’s credibility and personality. He seems to be ill informed that leads to untrue statements, and sometimes he just lies. There are websites that keep track of the many lies, outrageous statements, and the backing away of some of the promises, and statement he made during and after his election. Below are a few of them related to financial/economic topics:

“China is manipulating its currency.” The President-Elect was inferring that China was lowering its currency to have a price advantage in global markets. China was spending billions to keep its currency from falling, to help reduce capital flight. China was not lowering it, it was defending it. Most countries manipulate (protect) their currencies. The U.S. was accused of manipulating our currency by our trading partners during our Quantitative Easing period.

“I will self-fund my presidential election campaign” I was getting solicitations daily to help fund his campaign. He did have some high profile Wall Street and business people help him fund raise for his presidential campaign.

“I will be the greatest jobs president God ever created” One of his outrageous statements.

“Mexico will pay for the wall” The current and past two Mexican Presidents have all repeatedly said they will not pay for the wall.

“Can’t release tax returns due to audit” Very few people believe this excuse. This has led many people to guess, what is he trying to hide? Some suggest he is hiding that he doesn’t pay taxes, he isn’t as rich as he says that he is, he isn’t as charitable as he says he is, his ties to questionable countries, entities (Russia, mafia). He needs to release his taxes to do away with all the rumors, and to make sure there aren’t any conflicts of interest when he is running our country.

“It has not been easy for me. And you know I started off in Brooklyn, my father gave me a small loan of a million dollars.” There are several reports that say Trump was loaned much more over the years by his father. It’s also been reported that he benefitted from his father’s loan guarantees and connections.

“The unemployment rate is really 42%” maybe if you include children, retired people, the disabled, and others that aren’t and shouldn’t be included in unemployment reports.

“Obamacare. We’re going to repeal it, were going to replace it, get something great” We know now he does not have a plan to replace Obamacare.

“I’m worth $10 billion” Forbes magazine puts his net worth at about $3 to $4 billion, still very wealthy.

Forbes suggests that his assets may be worth about $10 billion but his net worth is closer to $4 billion.

If you can’t trust someone, can you really believe what they say and promise you? This will be a problem when dealing with our trading partners, allies, and foes.

He also tends to insult everyone in his path. Many leaders are saying to give him a chance. It’s up to the many groups he’s insulted to give him a chance including leaders from the left, right, intelligence agencies, and the media. He is making too many enemies.

Will our enemies and friends he’s insulted give him a chance including Mexico, China, Iran, North Korea, ISIS, and Muslims around the world?

I’m sure if President Elect Trump creates millions of high paying jobs for U.S. citizens, all will be forgiven here. A tall order, especially this late in the economic cycle.

The good news, some in his cabinet have opposite views of the President-Elect, and they could be a buffer between our trading partners, friends and enemies.

Summary

- The outlook for our economy for 2017 is positive.

- Investors are very enthusiastic regarding the new administration’s pro-growth, pro-business approach to governing.

- The markets are overvalued. I will have my 2017 Market Outlook posted in the near future.

- Interest rates, inflation, oil prices, and the dollar are all rising and they could challenge the markets and economy.

- The biggest risks to our economy and markets are outside our borders in terms of slow economic growth, terrorist attacks, and instability in the Middle East.

I remain cautious, patient and disciplined. Click here to read about my current investment strategy; it’s from my August Market Outlook.