The markets did well in 2017, and much better than most investors and analysts expected, including myself. My November Market Outlook tried to explain the unusual year. Click here to review the report.

I’m a value and contrarian investor, and every once in a while value investing is out on favor. Currently momentum investing (focus on earnings and price momentum) is more popular than value investing. Value investors try to determine the value of an asset and invest when their undervalued and sell/hedge when an asset is overvalued. The financial media is asking - is value investing dead? This question was also asked in the dot.com craze almost 20 years ago. Let’s assume you have a business you want to sell. Would you use technical/price analysis, or asset allocation to determine the price? NO YOU WOULDN’T. You would use discounted cash flows, or sum of the parts, or a multiple of a P/E or EBITDA to come up with a value for the company. Value, fundamental investing is not going out of style. Hard to imagine that it ever would.

I always provide the bullish case, but lately few people are looking at or factoring in the bearish case. Investors need to consider the bearish case and the risks to this economy and markets.

Bullish Case

- Investors and businesses are enthusiastic regarding the President and his administration’s pro-business actions including lowering regulations, and tax cuts for corporations and businesses.

- Capital spending has been increasing after being stagnant for much of this cycle.

- Capital spending picked up in 2017. The new capital spending accelerated tax deduction could help extend this trend.

- Earnings are expected to be up in 2018. See valuation section.

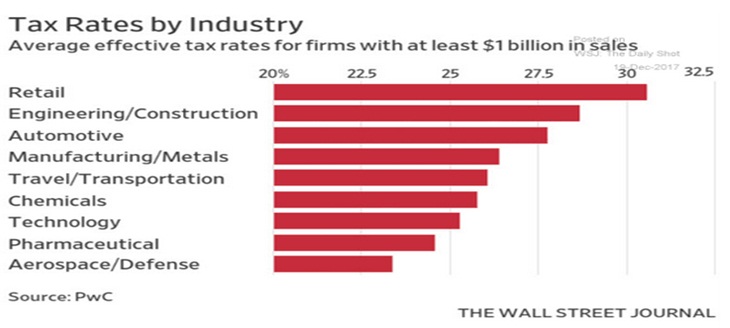

- The approved tax cuts will help certain industries more than others

The industries above should benefit the most from corporate tax cuts. Industries not listed have effective tax rates of 21% or below.

- Tax cuts and repatriation of corporate profits overseas could help investors with stock buybacks, dividend increases, more mergers and acquisitions.

Corporations allocated capital in the repatriation of overseas profits in 2004 by paying down debt, buying back stock, capital spending, mergers and acquisitions, and increased dividends.Stock buybacks, and mergers and acquisitions have been declining because of high stock valuations. We can expect less buybacks and mergers and acquisitions this late in the cycle.

Declining M & A is expected to continue.

Buying back stocks after an 8-year market rally with expensive valuations would not be a good idea for capital from tax savings.

- Many analysts point to a global synchronous growth that is helping our economy and our international companies. See overseas growth rates in the next section.

- Inflation and interest rates are relatively low

- The short-term technical underpinnings (sentiment, new highs, buying the dips) of this market are bullish. See technical analysis section.

- The cable financial news channels has many cheerleaders promoting the President’s economic agenda. It will be interesting to see if these same cheerleaders (Jim Cramer, Rick Santelli, Larry Kudlow, Stephen Moore, and the President’s economic team including Gary Cohn, Steve Mnuchin and Wilbur Ross) can shift from promoting tax cuts to getting corporations to hire more and raise wages. Some companies have announced one-time bonuses, but raising wages would be more helpful longer term.

- I would imagine that the next focus and promotion would be infrastructure spending. This could keep investors excited about the economy and markets. How infrastructure spending is financed, when it will occur (large projects will take several years to start) because of planning and regulations (especially at the state and local levels) and what infrastructure projects will be funded will determine the success of infrastructure spending.

- Declining supply of public companies to invest in

There about 50% less public companies to invest in today versus 1996. The top of the image provides the main reasons for the decline of public companies.

Bearish Case

- The markets are expensive and more than reflect the stimulus from tax cuts and deregulation.The strong market performance of 2017 will probably pull performance from 2018. More on this below in the Valuation section.

- I’ve read many market outlooks from many Wall Street firms and blogs, and the advice many investment professionals are giving to investors is: U.S. markets are too expensive, start shifting money into international markets.

- I’m constantly hearing on the cable financial news channels that one of the main reasons for the strong market is synchronous global growth. Below is a chart that shows that global growth did improve in 2017, but growth is expected to slow in 2018 except for an increase in growth for emerging markets and low income countries. There is a slight increase forecasted for the U.S. thanks to tax cuts:

The global growth rates of the major economies in the world are declining in 2018, not growing.

The P/Es for most economies have accelerated, and although they may have lower P/Es than the U.S., they also have lower growth and higher risks:

- The Euro stock index P/E has gone from about 7 to about 14, a double. Europe’s economy is expected to slow in 2018. Japan’s P/E looks reasonable, but its growth rate is expected to slow to less than 1%.

- Investors and analysts are not factoring in the many risks investors face. This market seems to focus more on the good news, and investors use any bad news and pullbacks to buy

- The market and investors are transitioning to a new era in the market where decision making becomes more automated (hedge funds, financial planners, 401K investors) and sectors and investment themes become crowded. These could lead to flash crashes that have happened in the past. Below is a chart of a dividend focused ETF:

- There was a flash crash in 2010 and 2015. Some analysts are concerned that this could happen again because most financial planners have their clients in these types of ETFs and many of these ETFs are crowded positions. If we have some intense selling, we could see more flash crashes.

- I went to a Blackrock (the largest money manager in the world, close to $6 trillion of assets under management) presentation on how they’re working on avoiding these flash crashes. Their strategies to minimize flash crashes are very complex. Blackrock has the talent, resources and technology to figure this out. If you own ETFs, ask the money manager of the ETF or your financial planner what safeguards they have if there is strong selling and/or to minimize the effects of flash crashes.

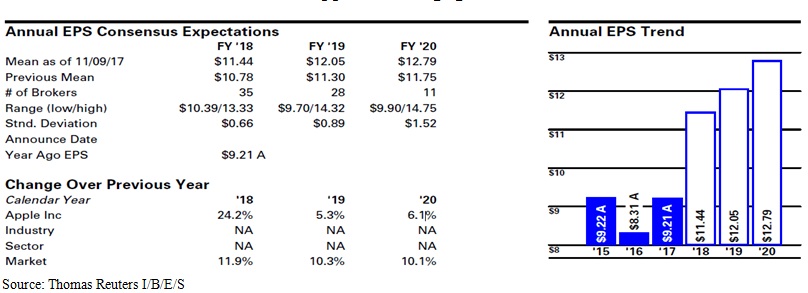

- Most analysts see the economy and earnings slowing in 2019 and beyond. What will happen to P/Es when growth slows later this year and into 2019? What happens when we have a recession?This could be a major problem for investors. Let’s look at an example, Apple:Here are the consensus forecasts for Apple’s earnings growth:

Source: Thomas Reuters I/B/E/S

Earnings are great this year, but slow dramatically the next two years. Will the P/E hold up?

- Apple’s P/E (forward four quarters) has jumped from around 11 to 16 in the last year. Will investors pay 16 times earnings for a company that’s growing about 6%? Most companies that are only growing mid-single digit don’t have P/Es of 16, and shouldn’t.Apple does have excellent products, services, and margins, but that’s more than reflected in the stock with a market capitalization of close to $900 billion.

- We are very late in this economic and market cycle. Some of the signs that this market and economy are in the late stages of this cycle include: full employment, rising interest rates and oil prices, high asset valuations, consumers are saving less and using their credit cards to keep up spending, quarterly earnings and economic indicator comparisons will get harder to beat after over eight years of recovery, continual rotation in the markets and a lack of leadership.

- Some point to FANG as the leaders in this market. Most leadership occurs during most of a market cycle. FANG has been strong since 2016. Also, there many articles in the financial press that governments around the world, including the U.S., will regulate more and issue more fines to FANG companies. The headline news and more regulations could weigh on FANG.

- Interest rates and oil prices are expected to continue to rise in 2018, a headwind for the economy

- Geopolitical threats including: North Korea, Iran, Syria, Venezuela, Russia, Islamists extremists groups (ISIS, Al Qaeda, Taliban, Boko Haram…). Also, Brexit is not going well and could cause dislocations in Europe and the rest of the global economy.

- If we look under the hood and the numbers regarding some of the conventional wisdom of the global economy and markets, we can see that the conventional wisdom is overstated (global growth and U.S. earnings growth) and is another reason why this market is overvalued.In the section above about global growth, we can see that that some investors and analysts are overstating the case for synchronous global growth.We look at earnings projections, P/Es and valuations in the valuation section below.

- Too many investors and Republicans believe that the tax cuts will be “rocket fuel” for the economy. Many economists and analysts don’t agree. Most analysts and economists believe that the tax cuts will give a small, short-term boost, but will create bigger problems with deficits and the growing national debt. The markets are probably getting ahead of itself in terms of the benefits of the tax cut. I included the chart below in my analysis of tax reform, click here to read the report.

The chart shows the multiplier effect (how many times when a dollar is spent will circulate in the economy.) We can see that corporate tax cuts have the smallest multiplier effect and is one of the reasons why economists are not expecting much improvement in GDP growth. Infrastructure spending does have a higher multiplier effect, if the infrastructure spending is done right. We don’t know if or when an infrastructure spending program will be passed this year. Infrastructure spending could be the next program that the Trump economic team can begin to promote to keep interest in the economy and the markets upbeat. The $1.5 trillion tax cuts will make an infrastructure program difficult to finance.

- Normally investors won’t pay a high P/E for earnings that have increased from inflation, tax cuts, or one-time events (asset sales). Investors tend to pay up for stocks that have above average growth rates and have true operating earnings. Investors should not be buying stocks with high P/Es because of tax cuts.

Also, if the tax cuts don’t create millions of high paying jobs (they probably won’t), then the Republicans could lose the House and Senate in November’s election as Trump supporters could become disappointed.

- The economy has never had this much fiscal stimulus this late in the cycle, especially tax cuts. If we fall into a recession, it will probably happen sooner than later, deficits could explode (less tax revenue due to tax cuts and a huge increase in unemployment insurance) and this will make the national debt much larger.

- If the dollar rises, it could be a problem for U.S. global competitiveness and lower the value of earnings for U.S. international companies.

- The Trump administration is under criminal investigation. There have already been a few convictions. Paul Manafort, Trump’s Presidential campaign manager, has been charged with conspiracy against the U.S., money laundering, tax evasion and lying. Mr. Manafort’s trial is set to start in May and he will fight the charges

- At a minimum, there is a question on the President’s choice of his staff members who have questionable backgrounds (General Michael Flynn, Paul Manafort, Steve Bannon, Steve Miller, and Sebastian Gorka). At worst he could wind up with charges like Manafort including collusion with the Russians and obstruction of justice. His military and economic teams are accomplished.

- Investors don’t seem concerned about the investigation. I heard one portfolio manager on CNBC state that it doesn’t matter because Vice President Pence would take over and the Republican economic agenda would continue. I doubt it would be that smooth, and most Trump supporters did not elect Vice President Pence, his priorities have more to do with his Christian faith. Also, political experts believe that Republicans could lose the House in the mid-term elections, making it more difficult to achieve the President’s economic agenda.

- Another concern that I have is President Trump has gone into bankruptcy more than once, partly because he does not understand economics, interest rate cycles, and he uses too much debt and risk. The tax bill that passed is very risky because we have large deficits and debt and we are late in an economic cycle. Also, interest rates may be reversing the long-term trend of declining interest rates. This cycle could end badly.

- Black and grey swan events (events that have a small probability of happening, but would have a significant impact on the economy and markets).

What Can Investors Expect in 2018

- The benefits of tax reform will diminish in 2019

- Growth comparisons will get more difficult in the 9th year of this cycle

- Higher interest rates and oil prices should start to be felt in the economy and markets

- As the economy and earnings slow and the age of the cycle becomes apparent, investors will realize the high valuations are not justified.

- Normally when a party is in control of the Presidency, the House and Senate, they will lose control of the House or Senate in mid-term elections, especially when the President’s approval rating are below 50. As I wrote above, it will be difficult to achieve the Republican economic agenda if they lose the House/Senate or both.

Valuations

Source: Barron’s, Thomas Reuters, Dan Hassey database

In late 2013, early 2014 earnings grew to about 1300 (4th column) and the P/E (fifth column) was about 13. Earnings went lower because energy prices collapsed, and China shifted from an investment, export and manufacturing focus to a service, consumer oriented economy. This led to a collapse in other commodity prices, and some resource rich countries (Australia, Brazil, Canada…) went into recessions that caused a slowdown in the global economy. Some of us thought that this could be the end of this economic and market cycle.

Earnings did recover to 2013 levels last year, and the P/E grew to 20. Most of the market’s performance has to do with P/E expansion. Why are investors willing to pay $20 for a dollar of earnings today, and only pay $13 for the same level of earnings in 2014?

Analysts have forecasted that earnings growth from 2017 and 2018 are double digits. If we take out the outliers and look at median earnings per share, EPS, forecasts, growth is more like 8%. Below is a table that has last year’s EPS (they are estimates but are probably very close to being the actuals because there is only one more quarter to report) and 2018 EPS forecasts:

Traveler’s Insurance, symbol TRV, will have the best earnings growth of the Dow 30 for 2018. TRV had terrible earnings last year because of the liabilities from hurricanes and fires. Its earnings are expected to recover this year (a big if, if there are no more major destructive weather events). Apple and Caterpillar were up substantially last year and have probably pulled price performance from last year that could impact price performance this year.

If we take the average of the earnings estimates, earnings are forecasted to be up about 10%. If we take the median earnings, they’re expected to be up about 8%. These numbers will change and is why I review them every week and include them in my monthly market updates.

It’s rare that earnings are up about 8% (median EPS for Dow 30) but the indexes are up over 20% like they were last year. Even with the anticipated tax cuts, the performance of the markets are not justified.

Below are my price targets for the markets:

Source: Barron’s Thomas Reuters

I use a P/E of 16 for the Dow 30 and 17 for the S & P, about the historical average. I’m a prudent, cautious investor in the late stages of cycle and with rising risks and interest rates. If we use a reasonable P/E, the markets are overvalued.

I doubt investors will take my advice. I’ve heard on CNBC from some portfolio managers that if investors are willing to pay $20 for earnings last year, they may be willing to pay $20 in 2018. If this is true, below is the potential for the markets in 2018:

Source: Barron’s Thomas Reuters

If earnings are met and P/Es stay elevated at 20, then there is some upside for the markets.

Are Tax Cuts Factored in the Markets and Stock Prices?

The above question is often discussed in the financial media. Some analysts and investors believe they are, some don’t.

My answer is earnings might not have adjusted enough yet (I’ve noticed that earnings forecasts have increased about 4% since the tax cut announcement), but prices certainly have.

If we look at the table on page 9, it shows the trend of earnings for this cycle. There was an earnings recession in 2015 and much of 2016. Once energy prices recovered, and the dollar went lower, earnings recovered. Earnings are up about 36% since 2016 but the market is up about 48%. Normally earnings growth and price appreciation are close. Because prices are up more than earnings, prices do probably reflect tax cuts and then some.

I will continue to monitor earnings forecasts and let readers know if earnings are improving or decreasing.

Below is a chart that compares the price performance of high tax rate companies and the S & P:

Source: The Daily Shot, Goldman Sachs

High tax companies were underperforming the S & P for much of 2017, but are now leading. Another example that tax cuts are reflected in prices.

Technicals

The technicals (price analysis) of this market are bullish, but there are a few red flags.Before I analyze the current market technicals, below is a chart that shows the seasonal tendencies of the market:

Source: www.erlangerchartroom.com

The above chart is a consolidation of 15 years of the Dow 30’s price action. The blue trends indicate rallies/buying tendencies. The orange trends indicate pullbacks/selling tendencies.

The seasonal tendencies of the markets include:

- Normally the market anticipates its prospects for the following year in November and most of the gains for the new year end around May. This is why some traders and investors “sell in May and go away.”

- In a bull market, the market is sensitive to quarterly earnings season. Normally the market anticipates earnings and rise in anticipation of a good earnings season. After the earnings season, investors tend to take profits and prices then consolidate until the next earnings season.

- September and October are normally the weakest months of the year.

Below is a current chart of the market:

Source: www.erlangerchartroom.com

Let’s review the chart:

Investors were enthusiastic about the new president and his pro-business agenda and the market had a parabolic move in late 2016. Also, once Donald Trump was elected his economic team was in full force on the cable financial news channels explaining and promoting their economic plans. Investors understood that the plan had a good chance of happening because Republicans controlled the Presidency, the House and Senate.

Once investors realized that the plan would take longer to implement than anticipated, the market started to act normal, similar to the seasonality chart above.

As the year progressed, investors started to realize that earnings were improving and there is synchronized global growth, and market action improved.

The first three consolidation periods, in rectangles, durations were normal, but the pullbacks were shallow. There was not much selling and investors and traders bought the pullbacks. As the year progressed the consolidation periods got shorter and there was little selling and investors bought the small pullbacks.

In my August Market Outlook, I explained that moves in prices normally move in about five steps and the market will normally retrace about 33% to 50% after the five steps. Often times these steps are the consolidation periods. Last year there was about 6 steps. This market will probably break this pattern.

The black trendline is the long-term trendline. Notice the acceleration from the trendline, the dotted trendlines. This is normally a sign of speculation.

Parabolic, 90 degree moves, are not sustainable, like most things in nature. Parabolic moves are also a sign of speculation. The last parabolic move in late November did not go far and ended in some selling. Investors used the selling to buy. Tax reform was passed in late December, and we have another parabolic move. We can probably expect this move to end soon, but investors and traders will probably use the selling to buy.

Another trend that is occurring in the markets is the automated buying from 401Ks (buying target funds), financial planners (buying ETFs) and hedge funds, and some portfolio managers. I’ve noticed the markets tends to gap up in the morning, but almost every day around the last hour before the market close, there is lots of buying. This probably means automatic buying by the participants listed. Below is a 5 day, 5 minute chart of the Dow 30 that shows the trend:

Source: schwab.com

I circled the openings and close of each of the five days. The only day where the market sold off in the last hour was the last day of the year, December 29. The selling was probably due to profit taking for 2017.

In the valuation section we reviewed the potential price targets for the markets. What do the technicals suggest may be the price targets for the markets? I tried to answer this question in my November Market Outlook. Here is an excerpt:

One of the main reasons why this market has been strong is because once prices break to new highs, most of the resistance and supply are gone, and it will be easy for prices to continue to make new highs. I rarely hear market analysts on cable financial news talk about this. Below is a long-term chart that shows the breakouts and new highs over the last 18 years:

Source: erlangerchartroom.com

- Let’s review the chart and breakouts:

- The Dow 30 was stuck below 11,500 from the late 1990s to 2006. Once prices broke above 11,500 the market was able to make new highs for about another year. Notice that after prices make new highs, many white candles are made. Many large candles show strength. This is true in each breakout, especially the breakout that started late last year.

- Prices were stuck below 14,000 from 2007 to 2013, and prices finally broke out to new highs. Prices were able to make new highs until 2015. Prices bottomed in 2009 at around 7000. There was supply resistance at 8000, 9000, 10000 to 14000. Once all the supply and resistance was taken out, prices were able to make new highs for a couple of years. Earnings growth and recovering economy, low interest rates and inflation also helped market performance.

- Prices were stuck below the 18,000 level from 2014 to 2016. Prices broke out to new highs in late 2016. Prices have been making new highs all year. We can expect prices to make new highs in 2018. How much more depends on earnings and if investors will be willing to pay. Also if we don’t have any grey or black swans.

- Normally when prices are making new highs, the next resistance level are round numbers. The next resistance levels for the S & P could be 2650, 2700, and for the Dow 30 it may be 23600, 23700, 23800….

The Dow 30 easily surpassed 25000 and is heading towards 26000; let’s see what happens at 26000, 26500, 27000…. The S & P surpassed 2700 and will probably breach 2800.

As I wrote about above, one of the reasons for the strength of the markets is global synchronous growth. Below is a chart that compares the performance and price action of the S & P, the foreign large cap ETF (symbol EFA is the 5th largest ETF in the world) and the emerging markets ETF (symbol EEM, the 14th largest ETF in the world):

Source: Yahoo Finance

The emerging markets ETF and big cap foreign stocks ETF outperformed the S & P last year.

Notice that the EFA and EEM did follow the normal pattern of stocks, a move and then a pullback/selling, especially the EEM. Again, investors and traders in domestic ETFs aren’t waiting for pullbacks in the markets. Since September, they seem to be buying on a daily basis.

Financial Planners have been plowing money into foreign stocks, this trend will probably continue this year.

I recommend not chasing this market. BE DISCIPLINED, BE CAUTIOUS, BE PATIENT.Below are the strategies I’ve been using.

My Current Investment/Trading Strategies

Here is my criteria for investing/trading in equities:

- Stock is in a bear market, down about 20%

- Prices found their low (when we move into a bear market, I will explain how this is determined).

- Prices are basing, trading sideways in their bear market (when we move into a bear market, I will explain more about the basing phase of a bear market).

- The stock pays an attractive dividend that has a history of growing, or the dividend is above 5%.

In my November issue I covered Occidental Petroleum (OXY ticker symbol), it does meet the above criteria. Below is a current chart:

Source: erlangerchartroom.com

Let’s review the chart:

- In 2014, OXY was over 100 and fell about 44%, bear market territory.

- Prices made a low in January 2016, and tested that low in the spring of 2017.

- Prices remain in its basing phase, from the high $50s to the $77.50 level. I’ve been investing with my clients in the low $60s.

- Currently, OXY is close to its resistance at $77.50. Oil prices normally go lower during the winter months because there is less travel because of the weather and refiners tend to do their maintenance and they buy less oil during this period. We will probably get another chance to add to our positions in the $60s this winter.

Because interest rates are rising, and expected to continue to rise, many dividend paying stocks are pulling back including utilities, REITS, bank loan/business development companies, and some consumer staple stocks.

- The tax cuts and deregulation should help the economy and markets in 2018

- Earnings estimates may not fully include the tax cuts, but stock and market prices do factor in tax cuts

- The markets are overvalued

- By mid-year the markets should be focusing on 2019 that has the potential of several headwinds (slower economic and earnings growth, high valuations, mid-term elections, rising interest rates and oil prices, geopolitical risks).

- Investors are not considering the risks investors face

- The markets are being dominated by automated decision making and buying by Financial Planners, 401K investors and algorithms by many portfolio managers and hedge funds.

- There are many signs that we are in the late phases of this economic and market cycle: valuations, new highs being made because the resistance/supply has been taken out, rising interest rates and oil prices, rotation in the markets and a lack of market leadership, full employment, the age of this economic and market cycle.

- My strategy is to focus on stocks that are in bear markets, pay an above average dividend, with a history of dividend growth.

- BE DISCIPLINED, BE CAUTIOUS, BE PATIENT.